featured

2026-06-12

Banking Trends

published

5 Minutes

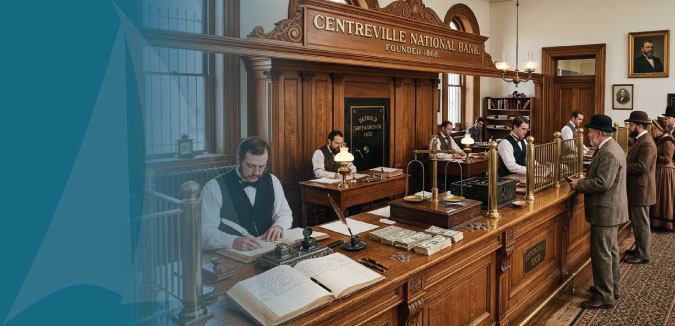

Imagine walking into a bank in the 1870s. There are no computers behind the counter, no debit cards in your wallet, and certainly no mobile apps letting you check your balance from home. Instead, the room is filled with the scratch of ink pens, the clink of coins, and shelves lined with massive handwritten ledger books. Banking in the late 19th century to early 20th century was slower, more personal, and deeply tied to trust and reputation.

While modern banking revolves around speed and digital technology, banking in the 1870s depended on people, paper, and physical memory. Yet many of the core functions that we rely on today, like saving money, lending funds, transferring payments, and protecting deposits, were already taking shape.

The Banking Landscape of the 1870s

The 1870s were an important period in American banking history. The country was still rebuilding economically after the Civil War, and lawmakers were working toward a more organized financial system. The National Bank act of 1863 had already introduced a national currency, helping to reduce confusion by banks printing their own money, but did not eliminate non-uniform currency immediately.

In 1875, bankers from across the country gathered in Saratoga Springs, New York, to form the American Bankers Association. The organization quickly became influential in shaping banking policy and advocating before Congress on issues affecting financial institutions.

Positions Inside the Bank

Bank staffing in the 1870s was much smaller than it is today. Most local banks operated with only a handful of employees, but each role carried major responsibility.

Cashiers

In the 1870s, the title “cashier” means something different than it does today. A bank cashier was often the second-highest authority in the institution, overseeing daily operations, supervising employees, and helping make lending decisions. In many cases, the cashier was effectively the operational leader of the bank.

Tellers and Clerks

Tellers handled deposits and withdrawals entirely by hand. Without calculators or software, strong mental math skills were essential. Accuracy mattered tremendously because one mistake in a ledger could throw off an entire day’s balancing process.

Clerks assisted with recordkeeping, correspondence, and maintaining ledgers. Every transaction had to be handwritten carefully in ink.

Bank Messengers

Many banks also employed messengers or runners, often young workers tasked with physically carrying documents, checks, or cash between businesses and banks. Since electronic communication was limited, these employees played an important role in daily operations.

Limited Security Staff

Security systems were minimal compared to modern standards. Most banks relied heavily on reputation, relationships, and community trust. While physical safeguards like vaults existed, armed guards (except for some cases, like in larger cities) and sophisticated fraud prevention systems were uncommon.

Documentation and Banking Tasks

Paperwork defined banking operations in the 1870s. Banks maintained enormous handwritten ledger books containing transaction histories, account balances, and loan records. Entire shelves could be filled with accounting books.

Checks were becoming more popular in the late 19th century, specifically among businesses and wealthier customers, though many Americans still relied primarily on cash transactions.

Without photo identification or digital security systems, banks would verify identity through personal recognition, introduction from trusted customers, and handwritten signature comparisons.

Fun fact: Shore United Bank still has old ledgers stored in the basement of the former Centreville National Bank dating back to 1876.

How Long It Took to Move Money

One of the biggest differences between banking then and now was speed. Today, money can move across the country in seconds. In the 1870s, transferring funds could take days or even weeks.

Local Transfers

Within a town, transactions might happen relatively quickly through paper checks or direct withdrawals. However, anything beyond the local area became far more complicated.

Mail and Rail Transport

Banks often moved money through mail delivery or railroad transportation. Drafts and payment instructions traveled physically between institutions, meaning distance greatly affected transaction speed.

A transfer from one state to another could take several days. International transfers could require weeks or months of waiting, depending on shipping routes and weather conditions.

Telegraph Banking

The telegraph represented one of the first major technological breakthroughs in banking communication. Some banks used telegraph systems to confirm transactions or verify balances, speeding up communication time, though actual settlement still required physical movement of funds. Although primitive compared to digital banking, it was revolutionary for the era.

Transporting Cash

Cash shipments were physically moved by horse-drawn wagons, trains, or stagecoaches. These shipments could become targets for theft and bandit attacks, especially in the more rural regions of the country.

How Banks Distributed Money

Modern banking revolutions around electronic transactions, but in the late 1870s banking was almost entirely physical.

Gold, Silver, and Paper Notes

Banks distributed money in the form of gold coins, silver coins and paper banknotes. Precious metals were extremely important because they backed much of the nation’s currency value under the gold standard, though at this time, the U.S. was not fully on a strict gold standard continuously due to the use of “greenbacks”.

“Greenbacks” were paper money issued by the government during the Civil War to support the economy when gold and silver were scarce. While first issued in 1861-1862, they remained in active circulation for decades but became redeemable for gold starting in early 1879.

Bank Notes from Individual Banks

Before full standardization, many banks issued their own banknotes. This created confusion because the value and trustworthiness of notes varied from bank to bank. Travelers sometimes carried counterfeit detection guides to determine whether unfamiliar notes were legitimate.

Lending Money in the 1870s

Lending practices were highly personal compared to today’s data-driven systems. Bankers often approved loans based on character and reputation rather than detailed financial analytics. A borrower’s standing in the community carried enormous weight.

Collateral was essential for receiving a loan. Most loans required collateral such as land, crops, inventory, livestock, or other goods. If borrowers failed to repay, the bank could seize the pledged assets.

Commercial Lending

Short-term commercial loans were common, especially for merchants, farmers, and businesses involved in trade. Loans frequently helped finance crop shipments or inventory purchases.

Early Mortgage Innovation

In the late 1800s, building and loan associations helped pioneer early amortized mortgage systems.

Saving Money in the 1870s

Savings accounts existed, but they were simpler by today’s standards. Customers used passbooks to keep track of deposits and withdrawals records by hand, but many Americans were skeptical of banks after financial crises such as the Panic of 1873, which caused widespread bank closures and economic hardship. Because deposits were not federally insured back then, losing savings in a bank collapse was a real risk.

Banking Then VS Today

The contrast between the 1870s and modern banking is dramatic. Here’s a quick overview of the many differences:

Speed of Transfers

1870s – Days or weeks

Today – Seconds or minutes

Banking Technology

1870s – Paper records or telegraphs

Today – Digital systems and Artificial Intelligence

Trust and Relationships

1870s – Personal face-to-face relationships

Today – Data, regulation, some face-to-face relationships

Access to funds

1870s – Local banks only

Today – Global access via apps and ATMs

Bank Security

1870s – Minimal fraud protection

Today – Encryption, biometrics, and monitoring

Lending Money

1870s – Reputation-based

Today – Credit scores and other financial information

Savings Accounts

1870s – Maintained by passbooks and handwritten entries

Today – Real-time digital balances

Currency

1870s – Physical coins and notes

Today – Mostly digital transactions via debit, credit cards and mobile apps

To summarize this, banking in the late 19th century was physical, local, and relationship based, while modern banking is more digital, global, and data driven.

A Foundation for Modern Banking

Although banking in the 1870s may seem slow and primitive compared to today’s standards, the era laid critical groundwork for the financial system Americans use today. National banking reforms, the formation of the American Bankers Association, the return to the gold standard, and innovations in lending all helped shape the future of banking.

The creation of the Federal Reserve System in 1913 would later transform the country’s scattered banking structure into a more coordinated national system capable of managing monetary policy and financial stability.

Even with today’s advanced technology, one important principle remains unchanged from the 1870s: banking is still built on trust. Whether transactions happen through a handwritten ledger or a smartphone app, customers continue to rely on financial institutions to safely manage their money and help them achieve their financial goals.

While trust is the foundation of any successful bank, it becomes even more meaningful when it has been earned over generations. A bank that’s been in operation since the 1870s reflects a deep-rooted commitment to the people, businesses, and communities that have made the journey possible. Learn more about what it’s like to work with a bank that has reached a 150 year milestone:

A LEGACY OF TRUST

Banking Trends

2026-05-18

At What Age Is My Child Ready for a Debit Card?

Read time: 4 Minutes

There comes a point in every child’s life when they start craving independence, and...

Community Banking

2026-04-29

150 Years of Banking: A Legacy of Trust

Read time: 3 Minutes

Reaching a 150-year milestone is no small achievement, especially in the world of b...

Community Banking

2026-03-31

How to Find the Best Bank Near You

Read time: 5 Minutes

Choosing the right bank is an important financial decision that can affect everythi...