Big enough to help. Small enough to care.

Stay updated on the latest news about our employees' participation in community projects and volunteer efforts with service organizations in our area. We're proud to highlight these activities because we strongly support nonprofit and charitable organizations that serve our communities.

04/01/2026

Cash Mobs

In 2025, we cash mobbed 29 businesses and gave away $16,473 to local businesses.

The Community Cash Mob is a group of Bank employees who visit a local business on a selected day and time to shop local with money on us to shop local!

Our 2026 Cash Mob Season is underway! Please check our Cash Mob page for updates.

In 2025, we cash mobbed 29 businesses and gave away $16,473 to local businesses.

The Community Cash Mob is a group of Bank employees who visit a local business on a selected day and time to shop local with money on us to shop local!

Our 2026 Cash Mob Season is underway! Please check our Cash Mob page for updates.

06/12/2026

.jpg)

Chris Gentry, Lainagail Greason, and Damian Garcia, along with a very special helper, Damian’s son Lucas, spent time giving back through a Culture Committee volunteer effort at Arundel Lodge, Inc.

The team rolled up their sleeves to help refresh the space with a fresh coat of paint

It is our honor to support an incredible organization dedicated to ensuring behavioral health challenges are not a barrier to living a meaningful life.

06/23/2026

Shore Leadership welcomed the community for an engaging evening at the Avalon Theatre for “Leadership and the American Experience.” Dr. Joe Thomas of the U.S. Naval Academy’s Stockdale Center for Ethical Leadership sparked meaningful conversation with his thought-provoking presentation on the role of leadership in shaping our nation.

04/24/2026

Shore United Bank was recognized as the Large Business of the Year at the Fredericksburg Regional Chamber of Commerce Gala. We are truly honored and appreciate the recognition that reflects the power of strong leadership and teamwork.

We couldn't have done this without the help of our incredible clients and communities. This award celebrates the strong relationships we have built, and the impact we strive to make every single day.

We couldn't have done this without the help of our incredible clients and communities. This award celebrates the strong relationships we have built, and the impact we strive to make every single day.

06/26/2026

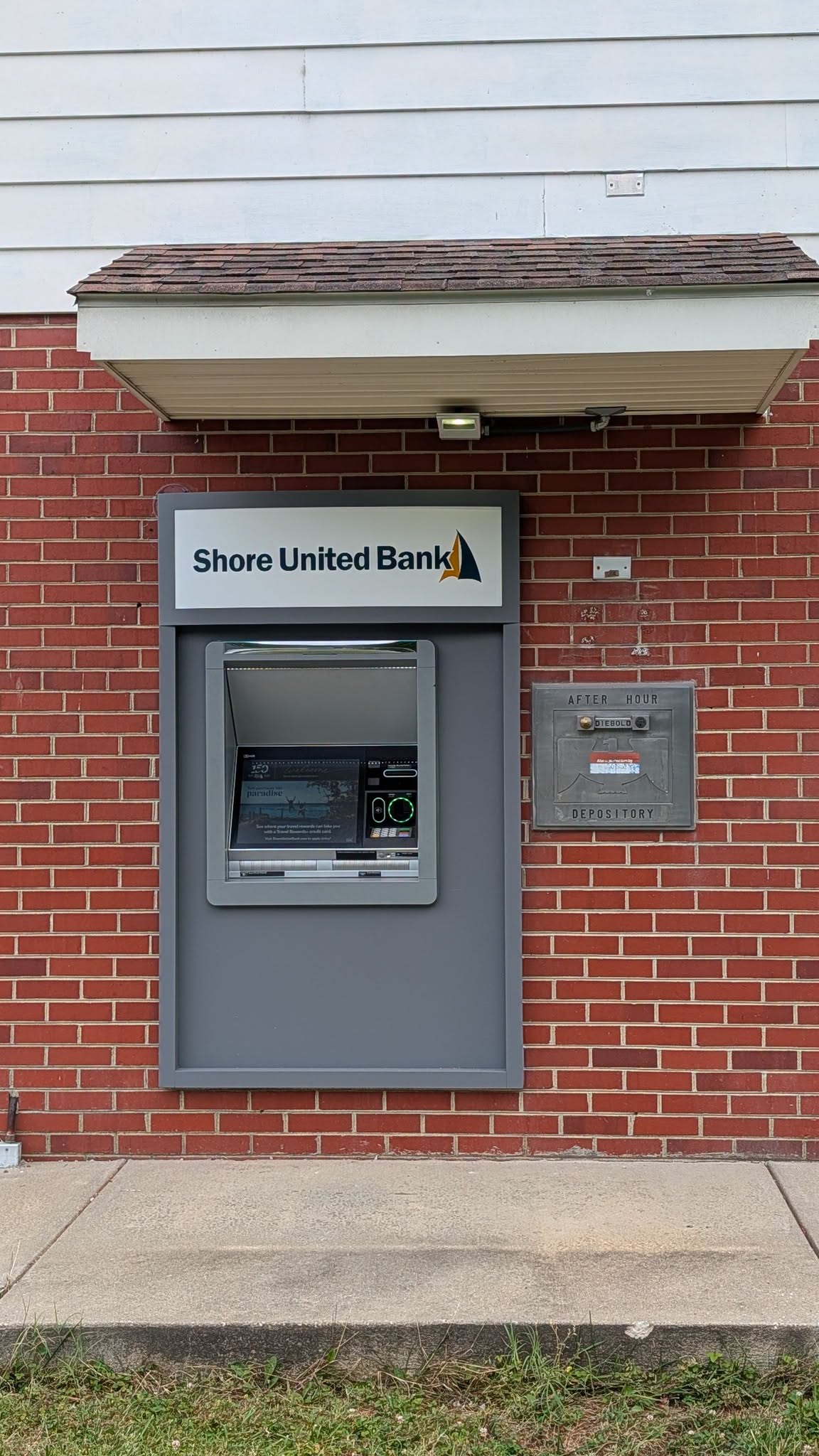

Shore United Bank opens a full-service ATM in Oxford, MD, located on 104 Factory Street.

06/28/2026

.jpg)

Cassie Stillwell, La Plata branch manager, graduated the Leadership Southern Maryland (LEAP) program

This incredible achievement highlights her dedication, leadership, and commitment to continuous growth. Her experience in LEAP strengthens both her impact on the team and the communities served.

06/02/2026

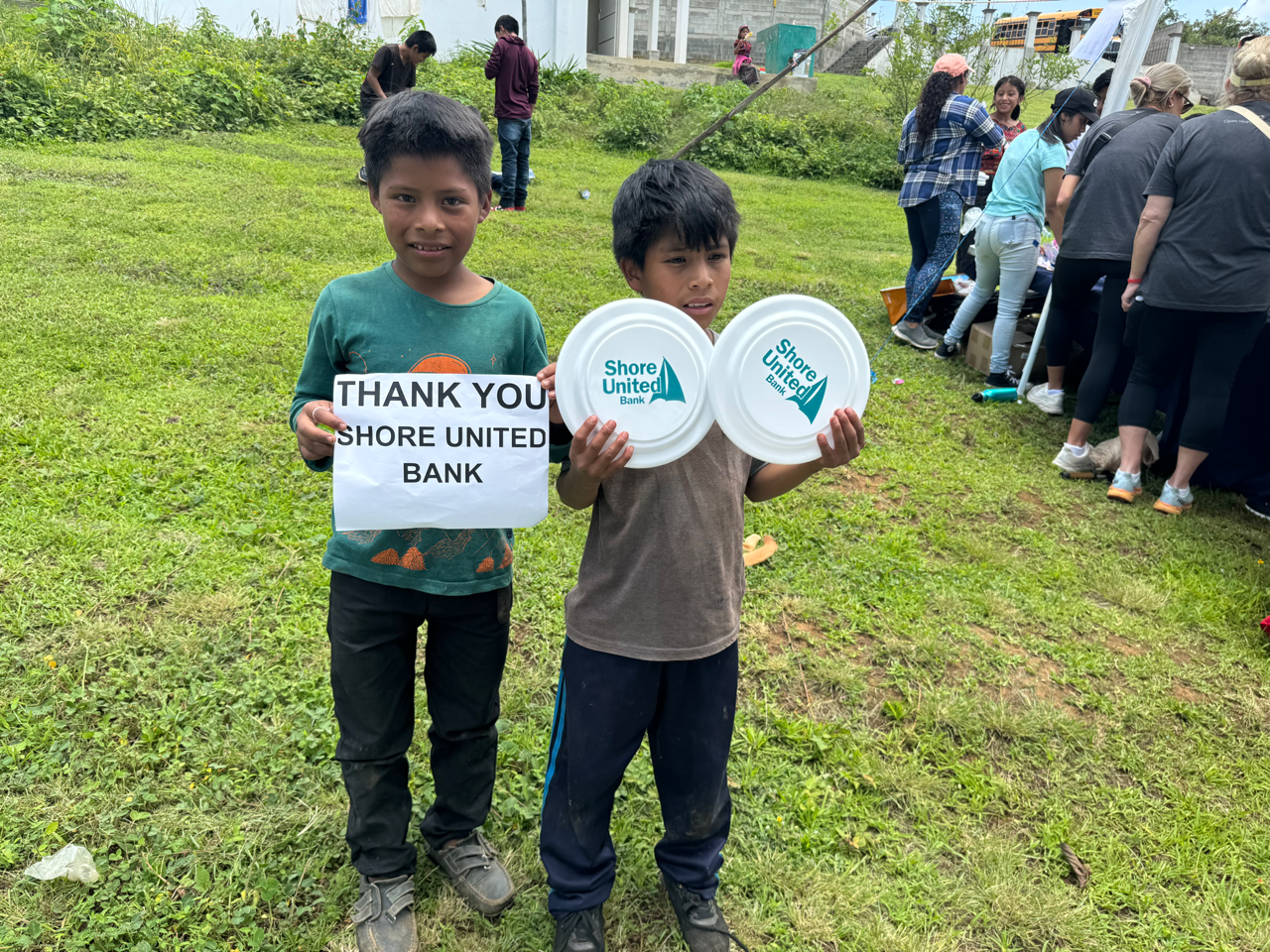

We were honored to support an inspiring mission led by our Stevensville branch customer, John VanWie, and his dedicated team as they traveled to Yalu, Guatemala.

United by a shared commitment to give back, the group provided essential resources such as bunk beds, stoves, and other meaningful improvements to the village.

We were proud to play a small part by donating frisbees for children at the local orphanage and throughout the community.

06/01/2026

Shore United Bank Attends Rally for our First Responders in Milton, DE

.png)

Logan Brayden and Aurora Berrios of our Rehoboth branch represented Shore United Bank at the 5th Annual Rally for our First Responders event in Milton, DE.

It is our honor and privilege to support the hard-working individuals that keep our communities safe.

It is our honor and privilege to support the hard-working individuals that keep our communities safe.

06/11/2026

.png)

Danielle Forrest and Joanna Barbee attended Career Day at Greensboro Elementary School.

They had the opportunity to connect with 3rd–5th grade students and share the many career paths available in banking, from customer service and lending to fraud prevention and financial literacy

05/19/2026

.jpg)

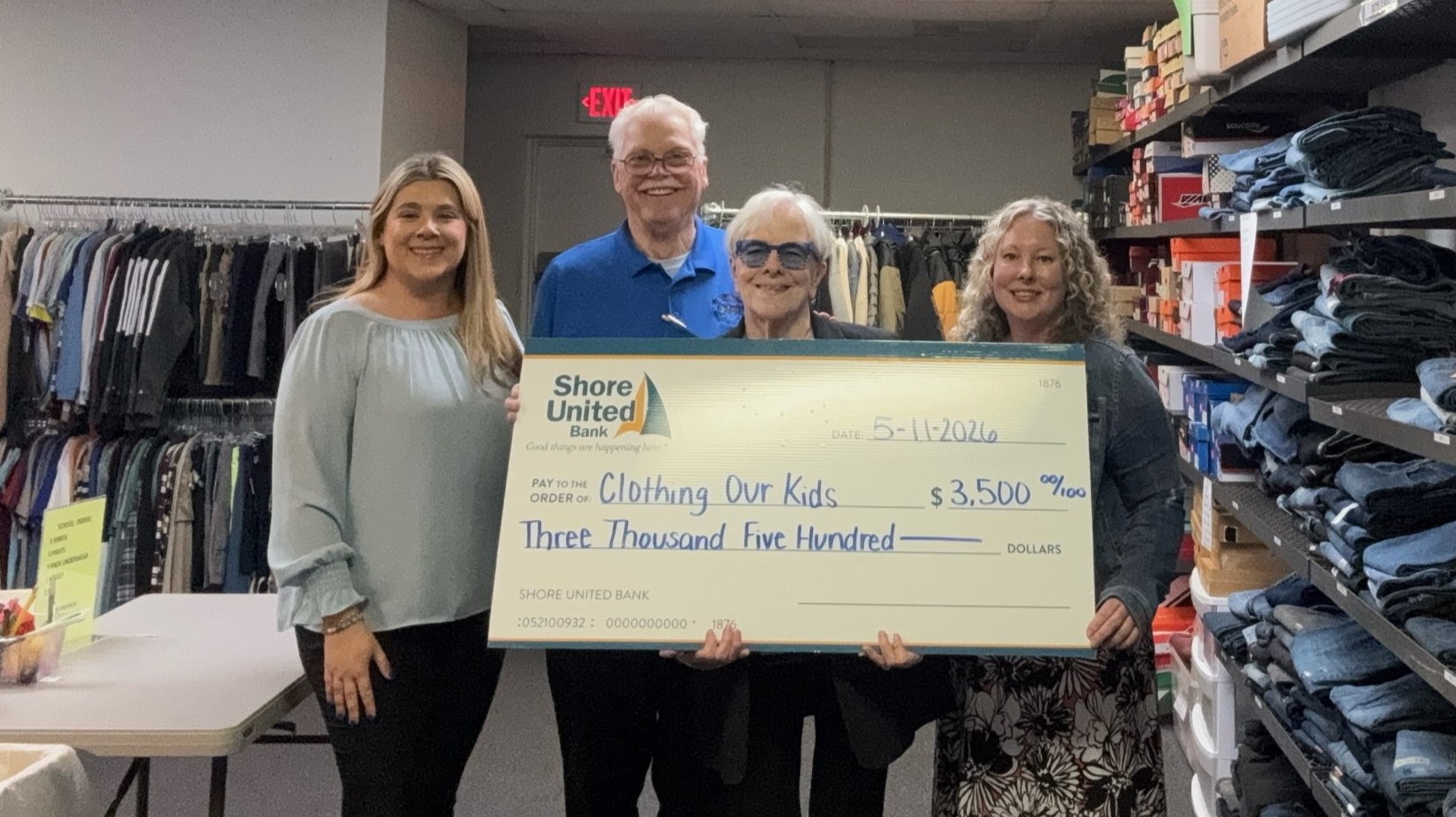

Our Rehoboth Beach branch recently made a charitable donation to Clothing Our Kids, an organization dedicated to providing essential clothing to children in need.

This contribution helps ensure local children have the confidence and comfort they deserve each day.

Thank you to Myndi and the entire Rehoboth team for making a meaningful difference in our coastal community.

07/02/2026

Steve Wientge Joins Shore United Bank as Relationship Manager

In this role, Wientge will be responsible for developing and managing commercial banking relationships, identifying lending opportunities, supporting business growth, and delivering financial solutions to clients throughout the region. He has more than 25 years of banking experience with a strong background in commercial lending, business development, deposit acquisition, and relationship management.

Most recently, Wientge served as Vice President, Commercial Lender at ACNB Bank, where he led business development efforts throughout Baltimore County and surrounding markets. He successfully increased commercial loan relationships by cultivating strong business connections, uncovering new lending opportunities through networking, and leveraging his in-depth understanding of local markets. Throughout his career, he has consistently demonstrated a commitment to customer service, responsible lending practices, and long-term client relationships.

04/23/2026

We’re excited to announce the opening of our new ATM located at 6204 Tilghman Island Road, Sherwood, MD 21665. This addition provides convenient access for our customers on Tilghman Island and surrounding areas. Whether you need to withdraw cash, check balances, or make deposits, our new ATM is ready to serve you—anytime, day or night.

07/01/2026

Chris Miles Joins Shore United Bank as Market Executive

In this role, Miles will be responsible for overseeing commercial banking relationships, expanding existing client portfolios, and supporting lending and deposit growth initiatives. He brings over 20 years of experience in banking and financial services, with a strong background in commercial lending, business development, and client relationship management.

Most recently, Miles served as Business Banker at First National Bank, where he developed and expanded business relationships, generated new lending opportunities, and consistently contributed to portfolio growth through strategic networking and financial analysis.

6/16/2026

Shore United Bank is proud to support, Rebuilding Together Eastern Shore with a $3,500 donation to help strengthen our local communities in Kent County.

This incredible provides critical home repairs and rehabilitation services for income-eligible seniors, veterans, individuals with disabilities, and families with children.

These funds will directly support projects in Kent County.

We’re honored to partner with organizations that share our commitment to community care and impact.

06/30/2026

.PNG)

Members of our Chesapeake South team recently volunteered at a Catholic Charities/Angel’s Watch homeless shelter in Charles County, supporting kitchen operations, and assisting residents.

It was a truly rewarding experience that highlighted the power of teamwork and community connection.

05/24/2026

Our Fredericksburg Team hosted a customer appreciation event at Ava Laurenne Bride - thank you to everyone who attended, as well as owners, Gabe and Wendy for allowing us to host an amazing event at their business.

06/30/2026

Relationship Manager, Sue Rollins was surprised by members of the Bryans Road VFD to honor her unwavering dedication, support, and commitment to their department.

03/03/2026

We are proud to share that Jimmy Burke, President and CEO, has been recognized as one of Maryland’s leading banking executives on The Daily Record’s 5th Annual Banking and Financial Services Power List.

Jimmy’s leadership continues to guide Shore United Bank with a clear focus on strategic growth, community impact, and a strong culture rooted in integrity and collaboration. This honor is not only a testament to his vision and leadership, but also to the collective work of our entire organization.

06/08/2026

This year marks an incredible milestone for our bank. 150 years of serving our communities, building relationships, and helping our customers achieve their financial goals. We’re proud of our rich history, but even more excited to celebrate the people who have made it all possible—our customers and our team members.