To develop a customized portfolio, we collaborate with each client taking you through the process to help you pursue your long-term financial goals.

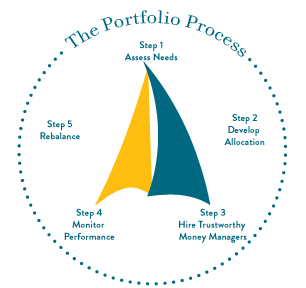

1. Assess Needs

We help our clients work towards their financial goals by adapting our services to fit your unique needs.

2. Develop Allocation

Our Advisors will walk you through a list of options available to help establish the risk tolerance that works for you and your family. Services available include:

- Mutual funds

- Fee-based portfolio Management

- Separately managed accounts

- Brokerage services through LPL Financial

- Cash management

- Alternative Investments

3. Hire Trustworthy Money Managers

- FCI Advisors

- DT Investment Partners

4. Monitor Performance

- Statement frequency as desired and 24/7 Online Access

- Monthly, quarterly, and/or annual performance reporting

- Ad-hoc reporting as requested (i.e. projected income, realized and unrealized gains and losses, tax worksheets, etc.)

- Regular face-to-face meeting with Wye Trust Advisors

5. Rebalance

- Analyze and reassess accounts

- Cash flow management

- Tax sensitive strategies

- Wealth transfer

- Collaborate with our professionals as requested by client